OECD Principles of Corporate Governance

The OECD Principles of Corporate Governance are among the most influential global frameworks guiding how organizations are directed, controlled, and held accountable. Developed by the Organisation for Economic Co-operation and Development (OECD), these principles were first introduced in 1999 and have since become an international benchmark for promoting transparency, fairness, accountability, and responsibility in corporate practices.

Designed to improve investor confidence and strengthen market integrity, the OECD framework serves as a reference point for policymakers, regulators, and corporations across both developed and emerging economies. Its global relevance lies in fostering trust between businesses, shareholders, and stakeholders—ensuring sustainable growth and ethical conduct in today’s interconnected markets. Check: Certificate in Corporate Governance, Risk & Compliance (GRC)

Closely aligned frameworks such as the G20/OECD Principles of Corporate Governance, the ICGN Global Governance Principles, and the ISO 37000 Governance of Organizations Standard build on similar values of transparency, ethical leadership, and accountability. Together, they provide a cohesive foundation for global governance excellence.

Understanding OECD Principles of Corporate Governance

The OECD Principles of Corporate Governance are globally recognized guidelines that define how corporations should be directed, managed, and held accountable. Established by the Organisation for Economic Co-operation and Development (OECD), these principles were originally introduced in 1999 to promote transparency, fairness, and efficiency across global financial markets.

Their purpose is clear: to strengthen corporate governance frameworks, protect investor rights, and ensure that companies operate responsibly in line with stakeholder expectations. Over the years, the principles have evolved to reflect changes in global economies and business landscapes. The most recent update—the 2023 revision of the G20/OECD Principles of Corporate Governance—modernized the framework by integrating emerging priorities such as sustainability, digital transformation, and ESG (Environmental, Social, and Governance) disclosure.

These principles are not limited to OECD member countries. They are designed to serve as a universal governance standard, guiding both emerging and developed markets. Nations around the world use them as a foundation for corporate law, regulatory frameworks, and governance reform.

By emphasizing accountability, transparency, and equitable treatment of shareholders, the OECD and G20/OECD Principles of Corporate Governance continue to play a vital role in shaping resilient, ethical, and sustainable corporate systems worldwide. Check: Strategic GRC Master Class Course

Key Objectives of the OECD Corporate Governance Framework

The OECD Corporate Governance Framework is designed to promote ethical, transparent, and responsible business conduct across global markets. It establishes a set of principles that guide organizations toward stronger accountability, investor protection, and long-term sustainability. The framework serves as a benchmark for both policymakers and corporations seeking to align with international best practices. Check: Fundamentals of Risk Management & Risk Champion Course

Core Objectives of the OECD Framework

- Promote Transparency and Accountability

- Encourage open communication between management, boards, and shareholders.

- Ensure that corporate decisions are traceable, measurable, and guided by integrity.

- Encourage Fair Treatment of Shareholders

- Guarantee equal access to information and voting rights for all investors, including minority shareholders.

- Protect against insider advantages or unfair practices that compromise shareholder trust.

- Strengthen Disclosure and Risk Oversight

- Improve the accuracy and timeliness of financial and non-financial reporting.

- Reinforce board-level oversight on emerging risks such as cybersecurity, ESG, and compliance.

- Support Sustainable Corporate Growth

- Align governance with long-term value creation, sustainability goals, and responsible investment principles.

- Help businesses balance profitability with environmental and social responsibility.

The OECD Principles of Corporate Governance provide more than just a compliance roadmap—they establish a culture of trust and accountability that strengthens economies. By focusing on transparency, fairness, and sustainability, these objectives enable companies to build resilient and ethical business models for the future.

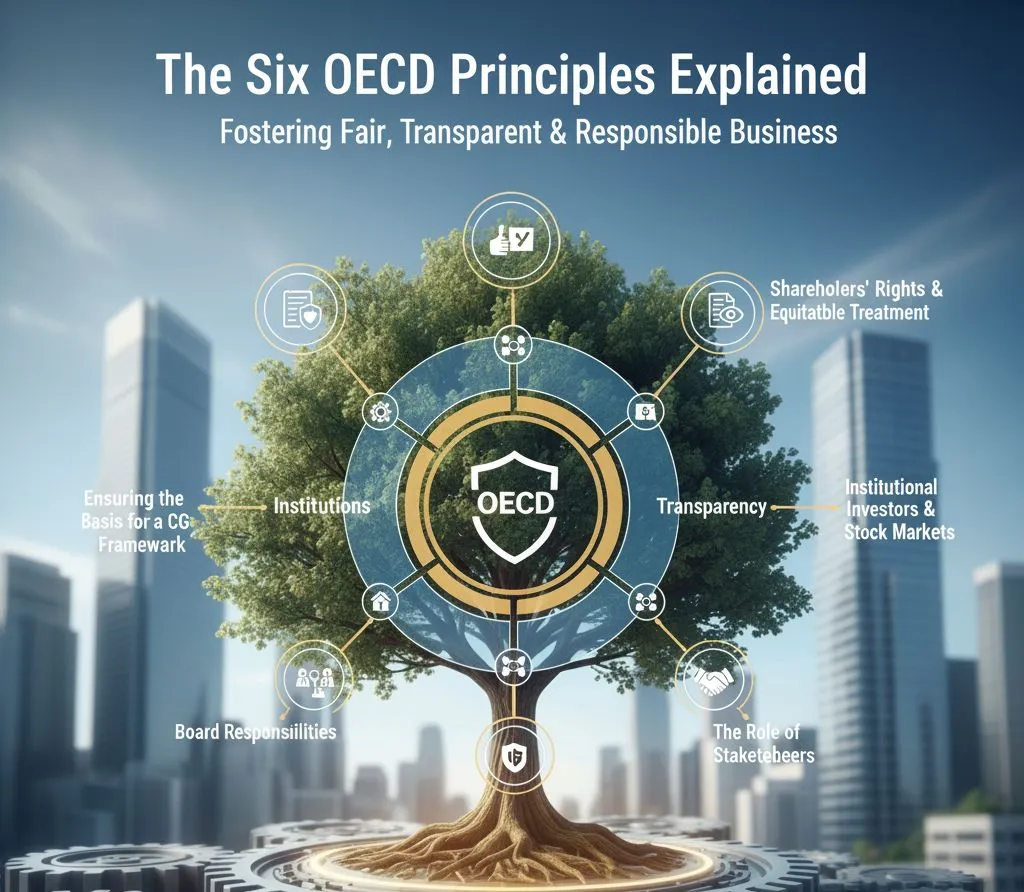

[caption id='attachment_28942' align='alignnone' width='1024']

The Six OECD Principles Explained[/caption]

The Six OECD Principles Explained[/caption]

The Six OECD Principles Explained

The OECD Principles of Corporate Governance outline six essential areas that guide countries and organizations in building strong governance systems. These principles are designed to promote transparency, accountability, fairness, and long-term value creation across global markets. Below is a breakdown of each principle, its purpose, and how it is applied internationally.

Ensuring the Basis for an Effective Corporate Governance Framework

This principle emphasizes the need for a robust legal, regulatory, and institutional framework that supports good governance. It ensures that markets operate transparently and that the rules governing corporate behavior are consistent, fair, and enforceable. Check: ESG Reporting Training Course

Real-world implication: Countries like Japan, Canada, and Brazil have reformed their governance codes based on OECD guidelines to improve investor confidence and market stability.

Global adoption: Many emerging markets use this principle as a foundation for aligning corporate law and regulatory oversight with international best practices.

Rights and Equitable Treatment of Shareholders

This principle focuses on protecting shareholder rights and ensuring equitable treatment of all investors, including minority and foreign shareholders. It promotes equal access to information, voting rights, and fair participation in key corporate decisions. Check: Certificate in Anti-Bribery and Corruption Compliance

Real-world implication: In the European Union, company law reforms ensure shareholders have stronger voting powers in executive pay and board appointments.

Global adoption: The principle has been adopted widely to prevent insider trading and to strengthen investor protection mechanisms.

Institutional Investors, Stock Markets, and Other Intermediaries

This principle highlights the role of institutional investors, stock exchanges, and financial intermediaries in promoting market integrity. It calls for transparency, stewardship, and accountability among entities that influence corporate behavior.

Real-world implication: Pension funds and sovereign wealth funds are increasingly required to disclose how they integrate ESG (Environmental, Social, and Governance) factors into investment decisions.

Global adoption: Stock exchanges in Singapore, London, and Dubai have adopted OECD-aligned listing requirements to strengthen governance among listed firms.

The Role of Stakeholders in Corporate Governance

This principle recognizes that good governance extends beyond shareholders—it includes employees, customers, suppliers, communities, and regulators. It encourages organizations to respect stakeholder rights and integrate them into governance decisions. Check: Certificate in ISO 37000:2021 - Governance of Organisations

Real-world implication: Many multinational corporations now publish sustainability and CSR reports, showcasing their commitment to ethical and responsible business conduct.

Global adoption: OECD-aligned countries promote social dialogue, employee participation, and stakeholder engagement in corporate decision-making.

Disclosure and Transparency

Transparency is one of the core principles of corporate governance under the OECD framework. This principle ensures that organizations disclose accurate, comprehensive, and timely information about financial performance, ownership, governance structures, and sustainability practices.

Real-world implication: Publicly listed companies in markets such as the U.S., U.K., and South Korea are required to adhere to detailed disclosure standards that align with OECD recommendations.

Global adoption: The principle supports investor confidence and market efficiency, forming the basis for frameworks like IFRS and G20/OECD disclosure guidelines.

Responsibilities of the Board

This final principle outlines the board’s role in guiding strategic direction, overseeing management, and ensuring accountability. Boards are responsible for aligning corporate objectives with shareholder and stakeholder interests while managing risks effectively.

Real-world implication: Many global companies have introduced independent directors and board committees (audit, nomination, risk) to ensure oversight integrity.

Global adoption: OECD-compliant governance codes in markets such as India, Saudi Arabia, and Australia emphasize board diversity, independence, and ESG accountability.

The G20/OECD Principles of Corporate Governance

The G20/OECD Principles of Corporate Governance represent a joint global effort to create a unified standard for responsible, transparent, and accountable corporate conduct. Originally based on the OECD framework introduced in 1999, these updated principles—endorsed by the G20 and the Organisation for Economic Co-operation and Development (OECD)—extend their influence beyond member nations to encompass the world’s largest and emerging economies. Check: Certified GRC Professional (GRCP) Training

Expanding the OECD Framework Globally

The G20’s involvement transformed the OECD guidelines into a truly international governance benchmark. By aligning corporate governance with the realities of global capital markets, the G20/OECD Principles of Corporate Governance help both developed and developing countries strengthen investor protection, improve board performance, and enhance financial market stability.

These principles promote:

- Global Consistency: Harmonizing governance policies across jurisdictions.

- Sustainable Growth: Encouraging long-term value creation through responsible business practices.

- ESG Integration: Embedding environmental, social, and governance standards into corporate strategy and reporting.

- Investor Confidence: Reinforcing trust through clear disclosure, accountability, and stakeholder engagement.

Updated Focus and Key Differences

The most recent 2023 revision of the G20/OECD principles introduced a sharper focus on digitalization, climate resilience, and ESG transparency—reflecting the evolving challenges businesses face in the 21st century. Unlike earlier OECD versions, the G20/OECD principles emphasize:

- Sustainability as a core governance objective.

- Digital transformation governance, including cybersecurity and data ethics.

- Global alignment, ensuring relevance to emerging markets as well as advanced economies.

Global Significance

Adopted by governments, stock exchanges, and financial regulators worldwide, the G20/OECD Principles of Corporate Governance have become the cornerstone for national governance codes and investor protection laws. Their inclusive approach bridges economies of different sizes and stages of development, reinforcing corporate integrity and supporting sustainable global market confidence.

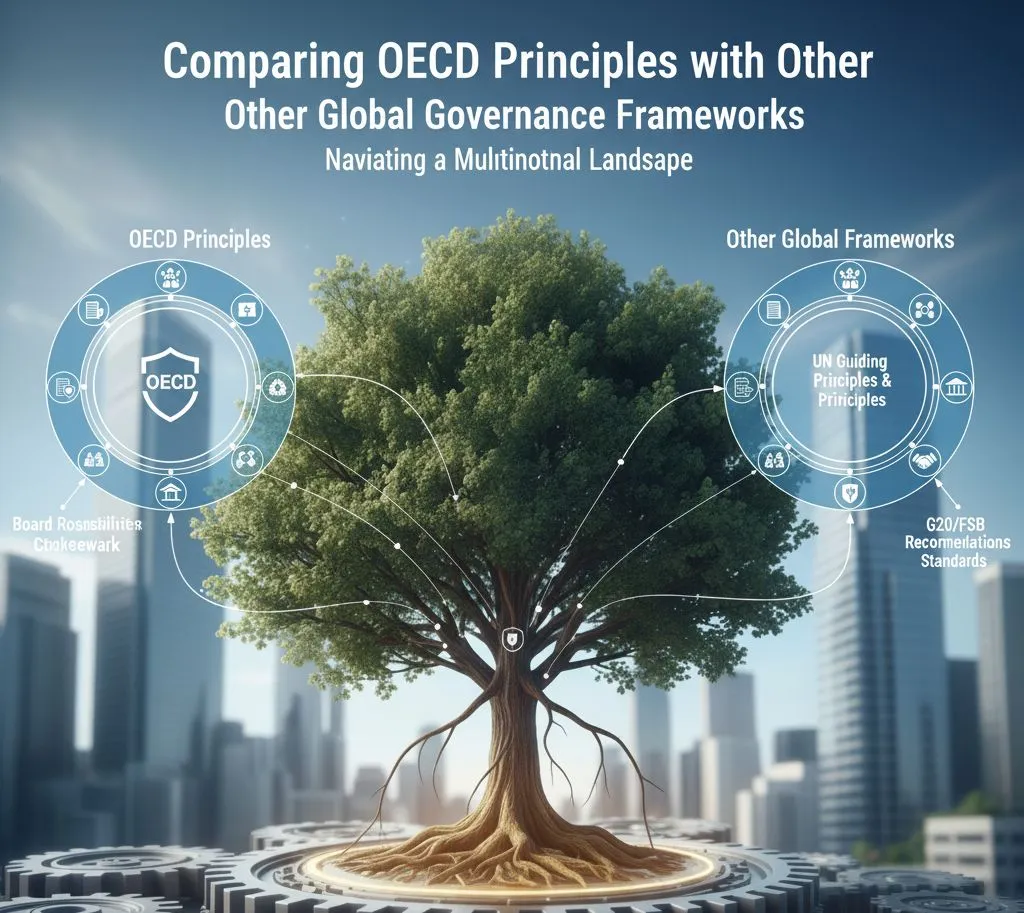

Comparing OECD Principles with Other Global Governance Frameworks

Global governance guidance doesn’t exist in a vacuum. The OECD Principles of Corporate Governance sit alongside other influential frameworks that emphasize stewardship, standardization, and jurisdiction-specific rules. Understanding how these frameworks relate helps boards apply best practice across markets and investor expectations. Below, we compare the OECD approach with investor-driven principles, an international management standard, and a comparison of corporate governance codes by country. Check: Certificate in ISO 37000:2021 - Governance of Organisations

ICGN Global Governance Principles

The ICGN Global Governance Principles (from the International Corporate Governance Network) complement the OECD by bringing a distinctly investor-focused perspective.

How ICGN complements OECD

- Investor stewardship: Elevates the role of asset owners and managers in engaging companies, voting responsibly, and promoting long-term value creation.

- ESG integration: Encourages investors to assess environmental, social, and governance risks/opportunities alongside financial factors.

- Board effectiveness: Reinforces expectations for board independence, diversity, and competence—aligned with OECD—but adds specific guidance on how investors evaluate these elements.

- Market accountability: Promotes transparent dialogue between companies and investors (e.g., disclosure clarity, rationale for board composition, capital allocation discipline).

Practical takeaway

- Use OECD as the policy and company-practice baseline; apply ICGN to understand how global investors will scrutinize strategy, capital stewardship, and sustainability.

ISO 37000 Governance of Organizations Principles

ISO 37000 frames governance as a management discipline with universal, principles-based guidance applicable to all organization types (listed firms, private companies, public bodies, NGOs).

What ISO 37000 adds

- Standardized terminology & structure: Clarifies roles, purpose, and accountability so governance can be implemented and audited within management systems.

- Purpose and outcomes focus: Aligns organizational purpose with stakeholder outcomes, ethics, and sustainable performance.

- Systemic integration: Embeds governance into strategy, risk, performance, and culture—useful for cross-border groups needing consistent practices.

Practical takeaway

- Combine OECD policy guidance with ISO 37000 to operationalize governance as repeatable processes, metrics, and continuous-improvement cycles.

Comparison of Corporate Governance Codes by Country

A concise comparison of corporate governance codes by country highlights how jurisdictions translate shared principles into rules and practices.

United Kingdom – UK Corporate Governance Code

- “Comply or explain” approach for listed companies; emphasizes board independence, audit/risk oversight, and stakeholder engagement (including the workforce).

- Strong focus on culture, accountability, and long-term success; flexibility allows boards to tailor practices with clear explanations to investors.

United States – Sarbanes-Oxley Act (SOX) & Listing Rules

- More rules-based and enforcement-heavy; mandates internal control reporting (Section 404), CEO/CFO certifications, audit committee independence.

- Emphasis on financial reporting integrity and auditor oversight (PCAOB); board independence and governance details also shaped by stock exchange rules (NYSE/Nasdaq).

Asia (selected examples)

- Japan: Corporate Governance Code promotes independent directors, stewardship, and capital efficiency (ROE focus), with growing attention to sustainability.

- Singapore: Code blends comply-or-explain with strong disclosure; highlights board renewal, independence, and risk management—aligned with regional investor expectations.

- India: SEBI regulations and Listing Obligations (LODR) set prescriptive requirements on board composition, related-party transactions, and enhanced disclosure, moving steadily toward global norms.

What differs—and what aligns

- Alignment: Board responsibilities, minority shareholder protection, disclosure/transparency, and risk oversight echo OECD themes across markets.

- Differences: The UK favors principles-based flexibility; the US stresses statutory controls and audit rigor; several Asian codes blend OECD concepts with local ownership structures, stewardship codes, and evolving ESG expectations.

Boardroom application

- Use OECD for universal anchors (shareholder rights, disclosure, board duties).

- Layer ICGN to anticipate investor stewardship demands.

- Implement ISO 37000 to embed governance as a measurable, organization-wide system.

- Localize with country codes (UK, US, Asia) to satisfy listing rules, enforcement realities, and cultural ownership patterns.

[caption id='attachment_28943' align='alignnone' width='1024']

Comparing OECD Principles with Other Global Governance Frameworks[/caption]

Comparing OECD Principles with Other Global Governance Frameworks[/caption]

Practical Application of OECD Governance Principles

The OECD Principles of Corporate Governance are not just theoretical guidelines—they serve as a practical framework that organizations use to enhance governance culture, strengthen accountability, and align with global investor expectations. Companies and regulators worldwide apply these principles to build transparent, ethical, and resilient governance systems.

How Companies Implement OECD Governance Standards

- Establishing Independent and Diverse Boards

- Strengthening Transparency and Disclosure

- Firms like Apple and HSBC publish detailed annual reports, ESG disclosures, and risk assessments—reflecting the OECD focus on transparency, disclosure, and stakeholder confidence.

- Protecting Shareholder Rights and Equality

- The London Stock Exchange and Tokyo Stock Exchange have both updated listing requirements to guarantee fair treatment and voting rights for minority shareholders, ensuring equitable participation in corporate decisions.

- Enhancing Risk Oversight and Internal Controls

- Financial institutions across Europe adopted OECD-inspired governance frameworks following the 2008 financial crisis, improving board-level risk committees and audit functions.

- Promoting Stakeholder Engagement

- Integrating ESG and Sustainability Reporting

- Under the revised G20/OECD Principles of Corporate Governance (2023), companies are now embedding sustainability and digital governance within their long-term strategies—demonstrated by leaders like Siemens, which links executive pay to ESG metrics.

Regulatory and Market Reforms

- Japan: The Tokyo Stock Exchange integrated OECD principles into its Corporate Governance Code to encourage independent directors and shareholder dialogue.

- India: SEBI’s Listing Obligations and Disclosure Requirements (LODR) mirror OECD principles, enhancing board independence and risk reporting.

- Saudi Arabia: The Capital Market Authority updated its corporate governance regulations in line with OECD recommendations to improve transparency and investor confidence.

Key Takeaway

Applying the OECD Principles of Corporate Governance enables organizations to transform compliance into culture—building trust, improving transparency, and ensuring long-term business resilience. Whether through regulatory reform or boardroom practice, these principles drive continuous improvement and sustainable corporate behavior across global markets.

Benefits and Challenges in Implementing OECD Principles

The OECD Principles of Corporate Governance provide a trusted foundation for improving business integrity, investor confidence, and sustainable growth. When effectively implemented, they strengthen governance culture across organizations and align national policies with international best practices. However, their adoption also comes with challenges—especially in markets with diverse regulatory, cultural, and economic conditions.

Key Benefits of Implementing OECD Principles

- Improved Investor Trust and Market Confidence

- By ensuring fairness, transparency, and accountability, organizations attract long-term investors who value strong governance practices.

- Example: Post-2008 reforms in European financial markets aligned with OECD principles, leading to enhanced investor protection and recovery of market credibility.

- Enhanced Transparency and Disclosure

- The framework promotes detailed, timely disclosure of financial and non-financial data, empowering stakeholders with accurate information for decision-making.

- Example: Listed corporations like HSBC and Siemens follow OECD-aligned disclosure policies that strengthen corporate reputation.

- Stronger Legal and Ethical Compliance

- Implementation supports adherence to anti-corruption, data privacy, and ESG regulations—key to maintaining organizational integrity.

- Sustainable and Long-Term Value Creation

- Companies that align with OECD principles tend to outperform peers in governance ratings, sustainability indices, and stakeholder satisfaction.

Common Challenges in Implementation

- Differences in Legal and Regulatory Systems

- Not all countries have the same enforcement mechanisms or legal maturity to uphold OECD standards.

- Emerging markets often lack the infrastructure or regulatory independence needed to ensure compliance.

- Market Maturity and Resource Gaps

- Smaller firms may find it difficult to allocate resources for governance reforms, audits, and reporting obligations.

- In contrast, mature markets typically integrate these principles more seamlessly through existing corporate laws.

- Cultural and Ownership Variations

- In regions with family-owned or state-controlled enterprises, decision-making can prioritize internal hierarchies over transparency or accountability.

- Cultural norms can influence board independence, whistleblower protection, and stakeholder engagement.

Balancing Opportunity and Complexity

Despite these challenges, adopting the OECD Principles of Corporate Governance remains essential for global competitiveness. By tailoring governance reforms to local contexts while maintaining alignment with international standards, organizations can enhance credibility, build investor trust, and ensure long-term operational sustainability.

Future of Corporate Governance Frameworks

The future of corporate governance frameworks is being shaped by rapid global transformation—driven by technological innovation, sustainability priorities, and a shift toward stakeholder-focused capitalism. Traditional governance models, once centered primarily on financial performance and shareholder returns, are now evolving to balance ethical responsibility, digital transparency, and long-term societal impact. Check: Strategic GRC Master Class Course

Evolving Priorities in Governance

- Environmental, Social, and Governance (ESG) Integration

- ESG has become a central pillar of corporate accountability. Governance now extends beyond financial oversight to include sustainability reporting, diversity, human rights, and climate resilience.

- OECD and ICGN frameworks increasingly emphasize ESG disclosure, linking it to risk management and investor trust.

- Ethical AI and Digital Governance

- The rise of artificial intelligence, automation, and data analytics introduces new governance responsibilities.

- Frameworks such as ISO 37000 and upcoming ISO/IEC AI standards focus on transparency, accountability, and ethical AI oversight to prevent algorithmic bias and misuse of data.

- Boards are expected to develop digital ethics policies that align with OECD guidance on AI and data governance.

- Stakeholder Capitalism and Inclusive Governance

- A growing shift from shareholder primacy toward stakeholder capitalism reflects the understanding that sustainable success depends on employees, customers, suppliers, and communities.

- The OECD and G20/OECD Principles of Corporate Governance (2023) now highlight stakeholder engagement and long-term sustainability as governance essentials.

Global Collaboration for the Digital Era

Governance is no longer a regional discipline—it is a global partnership. Organizations such as the OECD, G20, and ISO are working together to:

- Develop digitally adaptive governance frameworks that address cybersecurity, AI ethics, and data integrity.

- Harmonize ESG and sustainability reporting standards across jurisdictions.

- Build capacity for inclusive governance, ensuring that developing economies can align with global best practices.

The future of corporate governance frameworks lies in their adaptability. As the world transitions toward a digital and sustainable economy, frameworks like OECD, ICGN, and ISO 37000 will continue to evolve—integrating innovation, ethics, and sustainability into the very core of corporate decision-making. Organizations that embrace these future-ready principles will be better equipped to navigate risk, build stakeholder trust, and achieve long-term resilience.

FAQs on OECD Principles of Corporate Governance

-

What are the OECD Principles of Corporate Governance?

The OECD Principles of Corporate Governance are globally recognized guidelines that define how companies should be directed and controlled. They emphasize accountability, transparency, fairness, and responsibility to promote ethical business conduct and investor confidence.

-

How do the G20/OECD Principles differ from the original OECD guidelines?

The G20/OECD Principles of Corporate Governance expand the original OECD framework to a global level. They include stronger focus areas such as ESG integration, digital governance, and sustainability, ensuring that governance standards remain relevant in both developed and emerging markets.

-

What role do the ICGN Global Governance Principles play in corporate governance?

The ICGN Global Governance Principles complement the OECD framework by providing an investor-focused perspective. They promote responsible investment, long-term value creation, and stronger board accountability to meet the expectations of global shareholders.

-

How does ISO 37000 relate to OECD Principles?

ISO 37000: Governance of Organizations translates governance into a standardized management system. While OECD provides policy-level direction, ISO 37000 operationalizes these ideas by defining governance structures, responsibilities, and performance outcomes across all organization types.

-

Which countries follow OECD Corporate Governance Principles?

More than 60 countries—including OECD members and emerging economies such as Brazil, India, and Indonesia—align their national governance codes with the OECD Principles of Corporate Governance. The framework serves as a global benchmark for corporate and regulatory reform.

-

What are the benefits of adopting OECD Principles in organizations?

Adopting the OECD Principles of Corporate Governance helps organizations enhance transparency, strengthen board performance, improve investor relations, and ensure compliance with global standards—ultimately building long-term market trust.

-

How do OECD Principles promote sustainability and accountability?

The OECD framework encourages organizations to integrate ESG (Environmental, Social, and Governance) considerations into their strategy. It ensures that boards oversee climate, social, and ethical risks responsibly, fostering sustainable and accountable corporate growth.

-

What are the major differences in corporate governance codes by country?

The comparison of corporate governance codes by country shows that while OECD principles are universal, their application varies. The UK uses a “comply or explain” model, the US enforces strict rules through the Sarbanes-Oxley Act, and Asian markets balance regulation with cultural and ownership structures.